What Happens If You Don’t Pay Your Health Insurance Premium

Understand the severe risks of missing a health insurance payment, including retroactive cancellation and massive medical bills. Call (833) 877-9927 for expert guidance on your options.

By Nathaniel Crowley

Compare health plans

Finding plans in your area…

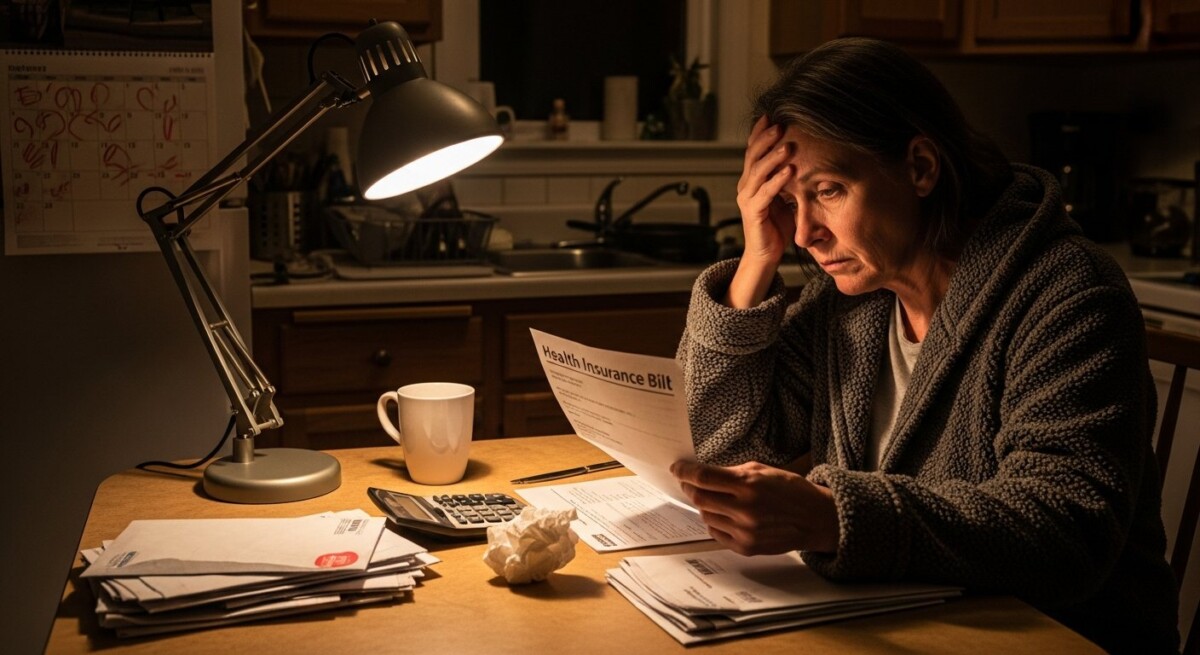

Missing a health insurance payment can feel like a minor oversight, but the consequences are often immediate and severe. Your coverage is not a subscription you can let lapse and easily restart. It is a financial contract, and failing to uphold your end, paying the premium, triggers a series of events that can leave you financially vulnerable and without access to care. Understanding the timeline and potential fallout is crucial for making informed decisions about your health and finances.

The Immediate Consequences of a Missed Payment

When your premium payment is late, the process is not instant cancellation. Health insurers, including those on the ACA Marketplace, are required to provide a grace period. This is a short window during which your coverage technically continues, but it is in a precarious state. For most plans purchased through the Health Insurance Marketplace, the grace period is 90 days if you are receiving an Advanced Premium Tax Credit (APTC) to help pay your premium. If you do not receive financial assistance, the grace period is typically much shorter, often 30 days or less, as dictated by your state’s laws and your specific policy terms.

During this grace period, your insurer is obligated to continue paying claims for the first month. However, if you do not pay the full past-due amount by the end of the grace period, your coverage will be terminated retroactively to the last day of the first month of the grace period. This means any claims incurred during the second and third months of a 90-day grace period could be denied, leaving you responsible for 100% of those medical bills. This retroactive cancellation is one of the most dangerous aspects of non-payment, as it creates a false sense of security that can lead to catastrophic debt.

Loss of Coverage and the Domino Effect

Once your coverage is officially canceled for non-payment, you are uninsured. This loss triggers several significant problems. First, you lose access to negotiated provider rates. Without insurance, you are billed the full “chargemaster” rate for any medical service, which can be several times higher than what an insurer pays. A simple urgent care visit or prescription can become unaffordable.

Second, you are exposed to financial ruin from a major health event. An accident, sudden illness, or emergency surgery can generate bills totaling tens or hundreds of thousands of dollars, potentially leading to medical bankruptcy. Third, you cannot simply re-enroll at will. Cancellation for non-payment does not qualify you for a Special Enrollment Period (SEP). This means you will likely have to wait until the next annual Open Enrollment period to get a new plan, leaving you unprotected for months. If you need guidance on when you can legally make a change, our resource on canceling health insurance anytime clarifies the rules.

Financial and Tax Penalties

The financial repercussions extend beyond medical bills. In the past, the federal tax penalty for not having health insurance (the individual mandate) was reduced to $0, meaning there is no longer a federal penalty. However, a handful of states, including Massachusetts, New Jersey, California, Rhode Island, and the District of Columbia, have implemented their own individual mandates with state-level tax penalties. If you live in one of these states and go without coverage for an extended period, you may face a fine when you file your state taxes.

Furthermore, if you received Advanced Premium Tax Credits to help pay your premiums and your coverage is terminated, you may have to reconcile this on your federal tax return. If your income for the year ended up being higher than you estimated when you applied for credits, you might owe money back to the IRS. The termination of your plan does not absolve you of this potential repayment obligation.

Options If You Cannot Afford Your Premium

If you are struggling to pay, taking proactive steps is far better than ignoring the bill. You have several avenues to explore before letting your policy lapse. First, contact your insurer or the Marketplace immediately. They may be able to help you update your application if your income has changed, which could qualify you for a larger subsidy and lower your monthly payment. You can also explore switching to a different plan within the same metal tier (like from a Gold to a Silver plan) that might have a lower premium.

If you have experienced a qualifying life event, such as a significant drop in income, you may be eligible for a Special Enrollment Period to change plans. Our article on changing health insurance mid-year details these events and the process. For those under 30 or who qualify for a hardship exemption, a Catastrophic health plan offers a much lower premium, though with a very high deductible. Finally, if your income is very low, you may qualify for Medicaid or the Children’s Health Insurance Program (CHIP), which have no or very low premiums and can be applied for at any time of the year.

Key steps to take if you cannot pay your premium:

- Contact your insurer or the Marketplace immediately to discuss your situation.

- Report any income changes, as this may increase your subsidy amount.

- Compare other available plans during a Special Enrollment Period if you qualify.

- Investigate eligibility for Medicaid/CHIP or a Catastrophic plan.

- Formally cancel your plan if you find alternative coverage, rather than letting it lapse for non-payment.

Reinstatement vs. Getting a New Plan

After cancellation for non-payment, some insurers may offer a reinstatement option if you pay all past-due premiums within a short timeframe after the grace period ends. This is not guaranteed and is entirely at the insurer’s discretion. Reinstatement is often more costly than finding a new plan, as you must pay for the months you were covered but did not pay, plus possibly fees.

Getting a new plan is your other option, but as mentioned, you are generally locked out until Open Enrollment unless you experience a qualifying life event. It is also important to understand that once your deductible resets, you start from zero. If you had already met a significant portion of your deductible on your old plan, that progress is lost. You can learn more about this financial dynamic in our explainer on what happens after your health insurance deductible is met.

Special Considerations for Different Plans

The consequences vary slightly depending on your insurance type. Employer-sponsored plans often have very short grace periods, sometimes only until the end of the month the premium was due. Your employer may also drop you from the plan quickly, as they are not obligated to keep you enrolled. For young adults, a common question arises about life events affecting dependent coverage. For instance, staying on a parent’s health insurance after getting married has specific rules that can affect your eligibility and premium responsibility. Medicare plans have their own strict rules, and losing Medicare Part B or Part D coverage for non-payment can lead to lifelong late enrollment penalties when you do re-enroll.

Frequently Asked Questions

How long do I have after missing a payment before my insurance is canceled?

If you receive a premium tax credit, you have a 90-day grace period. Otherwise, the grace period is typically 30 days or less, depending on your state and plan.

Can I get my health insurance back after cancellation for non-payment?

You may apply for reinstatement, but it is not guaranteed. More commonly, you must wait for the next Open Enrollment Period or qualify for a Special Enrollment Period to get a new plan.

Will I be penalized for not having health insurance?

There is no federal penalty, but some states have their own mandates and tax penalties for being uninsured.

What should I do if I know I cannot pay my next premium?

Do not wait. Contact the Health Insurance Marketplace or your insurer immediately to report an income change or explore switching to a lower-cost plan. Proactive communication is key.

Does non-payment affect my credit score?

Health insurers generally do not report late premiums to credit bureaus. However, if your unpaid premiums lead to medical debt that is sent to a collection agency, that collection account can severely damage your credit score.

Letting your health insurance lapse due to non-payment is a high-risk decision with layered consequences, from retroactive denial of claims to long periods without coverage. The safest path is always to communicate with your insurer or the Marketplace at the first sign of financial trouble to explore all available options for maintaining continuous, affordable coverage. Protecting your health and financial stability requires understanding these rules and acting before a missed payment becomes a crisis.

Compare health plans

Finding plans in your area…