Using Someone Else’s Health Insurance: Legal and Practical Guide

Using someone else’s health insurance is illegal and considered fraud. For legitimate coverage options and expert guidance, call our advisors at (833) 877-9927.

By Sabrina Lowell

Compare health plans

Finding plans in your area…

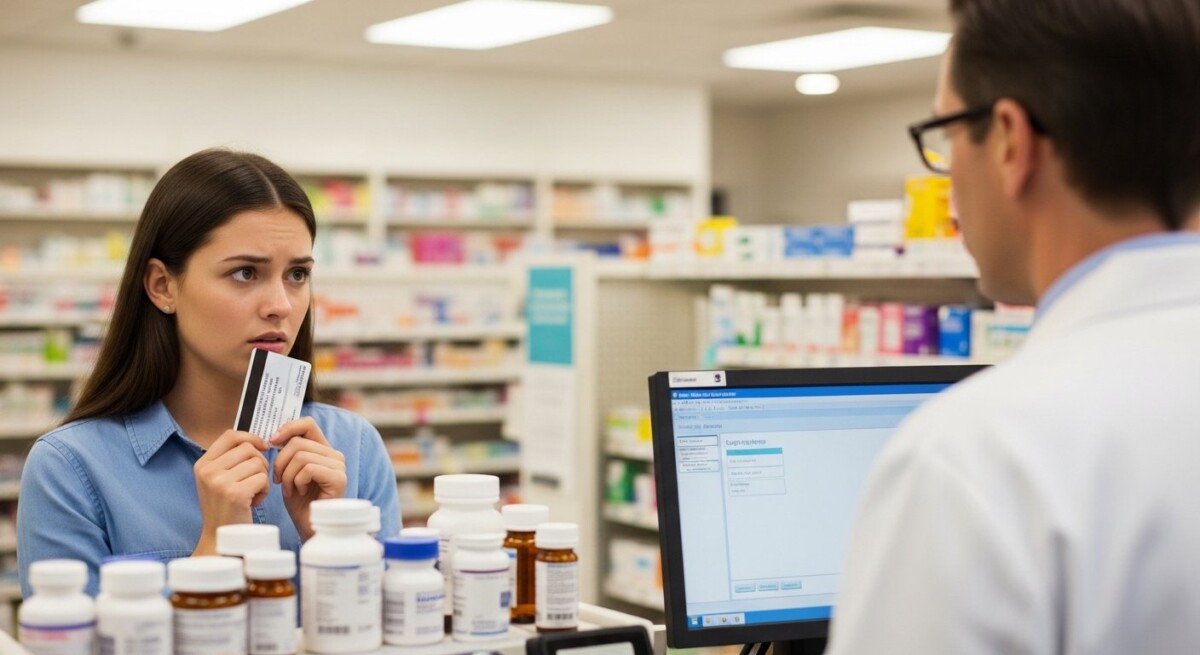

You are at the pharmacy counter, or perhaps checking in for a doctor’s appointment, and you wonder: can you use someone else’s health insurance? The short, critical answer is almost always no, you cannot legally use another person’s health insurance plan if you are not formally enrolled as a dependent or spouse on that policy. Health insurance is a contract between the insurer and a specific individual or group, and its benefits are not transferable like a coupon or a gift card. Using someone else’s insurance card constitutes fraud, a serious offense with potential legal and financial consequences. However, the question reveals a deeper need: understanding the legitimate pathways to gain coverage through another person, the rare exceptions that exist, and the correct actions to take if you find yourself uninsured.

The Core Rule: Insurance Is Not Transferable

Health insurance policies are legally binding agreements that explicitly name the covered individuals. These individuals are the policyholder (the primary subscriber) and their eligible dependents. The insurance company assesses risk and sets premiums based on the specific people listed on the application. Allowing anyone to use the policy would violate this fundamental contract. When you present an insurance card for services, you are attesting that you are the person named on that card. Misrepresenting yourself to receive healthcare benefits is insurance fraud. Providers verify eligibility, and discrepancies can lead to denied claims, demands for full payment from you, and even termination of the policyholder’s plan. Beyond the immediate bill, insurance fraud is a crime that can result in significant fines and imprisonment.

Legitimate Ways to Be Covered Under Another’s Plan

While you cannot simply borrow a card, there are established, legal mechanisms to become a covered member on someone else’s policy. This requires you to be added during an official enrollment period, provided you meet specific eligibility criteria set by the plan and, often, federal or state law.

Through Employer-Sponsored Plans

Employer-based health insurance typically allows employees to add dependents. The definition of a “dependent” is strict. It almost always includes the employee’s legal spouse and their biological, adopted, or step-children up to a certain age (usually 26). Some plans may also extend to children for whom the employee is a legal guardian. Importantly, you generally cannot add siblings, parents, grandparents, nieces, nephews, or unrelated friends to an employer-sponsored plan, even if you live with them and provide financial support. The rules for adding a dependent are not flexible, and you must do so during the plan’s annual Open Enrollment or within a Special Enrollment Period triggered by a qualifying life event, such as marriage or the birth of a child.

Through the Health Insurance Marketplace (ACA Plans)

Under the Affordable Care Act (ACA), the rules for dependents are similar but with a key focus on tax household composition. You can generally cover your spouse and children who are under 26 on a Marketplace plan. A crucial point is that, for ACA purposes, parents cannot be claimed as dependents on their adult children’s Marketplace plans, nor can adult siblings cover each other. Eligibility is tied to the tax filing relationship. If you are considering a major change in your coverage situation, it’s wise to understand your options, such as whether you can drop health insurance anytime without penalty, which is typically only during specific windows.

Through Government Programs (Medicaid, Medicare)

These programs have their own stringent eligibility rules based on age, disability status, income, and resources. Medicaid eligibility is individual, though household income is considered for the application. You cannot “use” someone else’s Medicaid benefits. Medicare is an individual entitlement; a spouse may qualify for Medicare on their own work record or potentially through their spouse’s record, but they must enroll separately. There is no sharing of Medicare cards.

Scenarios and Exceptions: When It Might Seem Possible

Certain situations create confusion, making it seem like using another’s insurance is acceptable. It is vital to clarify these gray areas.

First, a parent using their own insurance for a minor child is not “using someone else’s insurance”; the child is a verified dependent. The parent is the authorized representative managing the child’s benefits. Second, in a true medical emergency where the patient is unconscious or unable to communicate, a hospital will provide stabilizing treatment regardless of insurance. They will later work to identify correct coverage. Providing a family member’s insurance card at this point for a patient who is not on the plan is still fraudulent. The hospital will seek payment from the correct source once the patient’s identity is confirmed.

Another complex scenario involves coordination of benefits when a patient has two plans, such as through their own employer and as a dependent on a spouse’s plan. This is not using someone else’s plan illegitimately; it is a standard process where both plans you are rightfully enrolled in coordinate payment. Our detailed resource on how coordination of benefits works with two health plans explains the primary and secondary payer rules.

Risks and Consequences of Improper Use

The risks of attempting to use insurance you are not entitled to are severe and multi-faceted. For the person using the card, the immediate consequence is financial liability. The insurance company will deny the claim upon discovering the misrepresentation. The healthcare provider will then bill you directly for the full, undiscounted cost of services, which can be astronomically higher than the insurer’s negotiated rate. You may also be reported for fraud.

For the policyholder who knowingly allowed the use, the stakes are even higher. They risk having their entire policy canceled for material misrepresentation. They could face legal action from the insurer to recover wrongly paid claims, be subject to substantial fines, and potentially face criminal charges. Furthermore, they may find it difficult and expensive to obtain health insurance in the future. It is critical to know that being denied health insurance or having a policy rescinded for fraud creates a long-lasting record.

What to Do If You Need Coverage

If you are asking this question because you lack insurance, focus on legal avenues to obtain it. Here are your primary options:

- Marketplace Special Enrollment: Losing other coverage, getting married, having a baby, or moving are examples of Qualifying Life Events (QLEs) that trigger a 60-day window to enroll in an ACA plan.

- Medicaid/CHIP: These programs offer free or low-cost coverage and have year-round enrollment if you meet income and other eligibility criteria.

- Employer Plans: If you start a new job, you typically have a limited window to enroll in your employer’s plan.

- COBRA: If you lose job-based coverage, COBRA allows you to continue the same plan for a limited time, though you pay the full premium.

- Short-Term Plans: These can provide temporary, limited coverage but do not offer the comprehensive benefits or protections of ACA plans.

Once you secure legitimate coverage, understanding your benefits is key. For instance, knowing what happens after your health insurance deductible is met helps you plan for subsequent medical costs within the same year.

Frequently Asked Questions

Can I use my boyfriend’s/girlfriend’s or domestic partner’s health insurance?

Unless the plan specifically offers and defines domestic partner coverage (and you meet all requirements for documentation), and you are officially added during enrollment, the answer is no. Marriage is the nearly universal requirement for spousal coverage.

Can I use my parent’s insurance if I am over 26?

No. The ACA mandate allowing children to stay on a parent’s plan ends at age 26. Your only exceptions would be if your state has an extended age requirement or if you are disabled and qualify as a dependent. You must seek your own coverage.

What if I just use it for a prescription? It’s a small thing.

Insurance fraud is not measured by the size of the claim. Using another’s benefits for any service, including a pharmacy prescription, is illegal and can be detected through pharmacy benefit management systems.

Can I bill my child’s expenses to my plan if they are on their own plan?

If your child has their own insurance as the primary policyholder, that plan is primary. Your plan may provide secondary coverage if they are still your eligible dependent. You must coordinate benefits correctly, not choose which card to use.

What should I do if a provider’s office asks to copy my insurance card for my adult family member who lives with me?

You should politely but firmly clarify that the family member is not covered under your policy. Provide their own insurance information if they have it, or state that they will be self-pay. Do not hand over your card.

Navigating health insurance rules can be complex, but understanding the fundamental principle that coverage is non-transferable protects you from severe repercussions. Always pursue legitimate enrollment pathways during designated periods. If you are uninsured, explore Marketplace options, Medicaid eligibility, or employer-based coverage. Protecting your financial and legal health is just as important as addressing your medical needs, and using insurance correctly is a cornerstone of that protection.

Compare health plans

Finding plans in your area…