The Real Cost of Being Uninsured in 2026

Understand the severe financial and medical risks of being uninsured. For personalized guidance on your 2026 options, call (833) 877-9927.

By Elliot Kingsley

Compare health plans

Finding plans in your area…

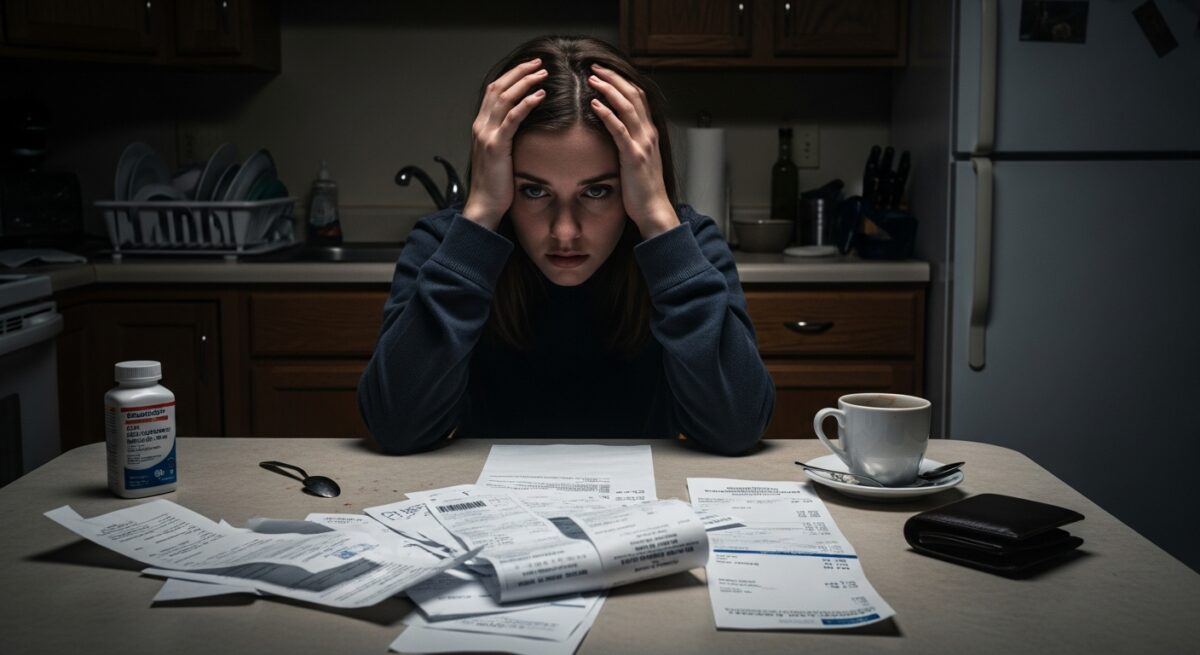

Facing a medical emergency or even a routine doctor’s visit without health insurance is a daunting financial prospect. While the federal individual mandate penalty is no longer in effect, the personal consequences of being uninsured remain severe and multifaceted. As we look ahead to 2026, understanding these risks is crucial for making an informed decision about your coverage. The landscape of healthcare costs, legal frameworks, and personal financial vulnerability creates a perfect storm for those who gamble on going without a safety net.

The Financial Fallout of Medical Debt

Without health insurance, you are responsible for 100% of your medical bills. In 2026, with healthcare inflation consistently outpacing general inflation, these costs will be higher than ever. A single trip to the emergency room for a broken arm can easily exceed $7,500. A three-day hospital stay averages over $30,000. For serious conditions like cancer or heart surgery, bills can soar into the hundreds of thousands. These are not hypotheticals, they are the stark reality for the uninsured. Hospitals are required to stabilize patients in emergencies regardless of ability to pay, but they will absolutely bill you for the full, undiscounted rate afterward. This often leads to medical debt, which is the leading cause of personal bankruptcy in the United States. Unlike other forms of debt, medical debt can accumulate suddenly and catastrophically, with little warning.

Furthermore, you lose access to the negotiated rates that insurance companies have with providers. An insured patient might pay a $150 copay for an MRI that is billed at $2,500, with the insurer paying the discounted remainder. An uninsured patient receives a bill for the full $2,500. This lack of leverage makes every medical interaction a potential financial crisis. To manage costs, you must proactively seek out pricing, which is often opaque and difficult to obtain, and negotiate directly with providers, a stressful and uncertain process.

Limited Access to Care and Preventative Services

Beyond the financial shock, being uninsured severely limits your access to non-emergency healthcare. You are far less likely to seek preventative care, such as annual physicals, cancer screenings, vaccinations, and management of chronic conditions like diabetes or high blood pressure. This leads to a dangerous cycle: minor, treatable issues are ignored until they become major, expensive health crises. For example, managing diabetes with regular check-ups and medication is far less costly than treating kidney failure or a foot amputation resulting from unmanaged disease.

Finding a primary care doctor or specialist willing to see an uninsured patient can be challenging. Many practices require upfront payment or deposits from self-pay patients. This barrier means necessary care is often delayed or forgone entirely, resulting in worse health outcomes. The consequences are not just physical, the constant stress of knowing you are one illness away from financial ruin can take a significant toll on mental health.

The 2026 Landscape: Mandates, Penalties, and Subsidies

It is critical to understand the current legal and assistance framework. The federal tax penalty for not having health insurance, known as the individual mandate, was reduced to $0 starting in 2019. However, a handful of states and the District of Columbia have implemented their own individual mandates with state-level penalties. As of now, these include Massachusetts, New Jersey, California, Rhode Island, and Washington D.C. If you live in one of these jurisdictions, you could face a state tax penalty for being uninsured in 2026. These penalties are often calculated as a percentage of household income or a flat fee per adult, whichever is higher.

On the supportive side, the enhanced premium tax credits (subsidies) created under the American Rescue Plan and extended by the Inflation Reduction Act are currently set to expire at the end of 2025. Their status for 2026 is a key political question. If they are not renewed, the cost of marketplace plans will rise significantly for millions of Americans. However, if they are extended or made permanent, robust financial assistance will remain available to lower the monthly cost of insurance for those who qualify based on income. Staying informed on this policy issue is essential for planning your 2026 coverage.

To navigate this complex system and find an affordable plan, a strategic approach is necessary. Our dedicated resource on finding the best health insurance for your needs in 2026 breaks down the steps to evaluate plans, maximize subsidies, and choose the right coverage for your situation.

Practical Consequences and Long-Term Risks

The day-to-day and long-term impacts of being uninsured extend beyond immediate bills. Consider these tangible risks:

- Credit Score Damage: Unpaid medical bills are frequently sent to collections agencies, which then report the debt to credit bureaus. This can devastate your credit score, making it harder to secure loans, rent an apartment, or even get certain jobs.

- Wage Garnishment and Liens: If a medical provider or collections agency wins a lawsuit against you for unpaid debt, they may be able to garnish your wages or place a lien on your property.

- Barriers to Future Coverage: While the Affordable Care Act prohibits denial of coverage for pre-existing conditions, you can only enroll during the annual Open Enrollment Period or a Special Enrollment Period triggered by a qualifying life event. An unexpected diagnosis while uninsured does not create a Special Enrollment Period, potentially locking you out of comprehensive coverage until the next Open Enrollment.

- Full Financial Exposure: You bear the entire risk. There is no annual out-of-pocket maximum to protect you. A serious accident or illness could generate bills that eclipse your lifetime savings, retirement funds, and children’s college funds.

Exploring Your Coverage Options for 2026

Given the severe risks, exploring all avenues for coverage is imperative. You are not limited to traditional employer-sponsored plans or expensive individual policies. Several pathways exist, each with its own eligibility criteria and cost structure. A comprehensive review of all available options is the first step toward securing protection. For instance, while most auto insurers like Geico do not underwrite major medical plans, understanding what types of coverage are available through different channels is key, as explained in our analysis of whether Geico has health insurance.

Your main options typically include:

- The Health Insurance Marketplace (Healthcare.gov or State-Based Exchanges): This is where you can shop for Qualified Health Plans (QHPs) and access premium tax credits and cost-sharing reductions based on your income. Open Enrollment for 2026 coverage will likely occur in late 2025.

- Employer-Sponsored Insurance: If available through your or a spouse’s employer, this is often a cost-effective option, with the employer subsidizing a large portion of the premium.

- Government Programs: Medicaid (based on income and state expansion rules) and Medicare (for those 65+ or with qualifying disabilities).

- Catastrophic Health Plans: Available to those under 30 or with a hardship exemption, these plans have very low premiums but very high deductibles, designed to protect against worst-case scenarios.

- Short-Term Limited Duration Insurance: These non-ACA-compliant plans can provide temporary, low-cost coverage for specific gaps but exclude pre-existing conditions and offer limited benefits.

Frequently Asked Questions

Is there a federal penalty for not having health insurance in 2026?

No, the federal tax penalty is $0. However, you should check if your state has its own individual mandate and penalty.

Can I be denied care in an emergency if I’m uninsured?

No. Federal law (EMTALA) requires hospital emergency departments to stabilize any patient with an emergency medical condition, regardless of insurance or ability to pay. However, you will be billed for the full cost of that care afterward.

What if I’m young and healthy? Do I really need insurance?

Accidents and unexpected illnesses do not discriminate by age. A serious bike accident, appendicitis, or sudden diagnosis can happen to anyone. Insurance is fundamentally about managing unforeseen risk.

How can I afford insurance if I don’t qualify for subsidies?

Explore all plan tiers (Bronze, Silver, Gold) on the Marketplace. Consider a High-Deductible Health Plan (HDHP) paired with a Health Savings Account (HSA) for tax advantages. Also, investigate whether you qualify for a Catastrophic plan or if a professional association offers group rates.

What’s the single biggest mistake people make when uninsured?

Assuming that because they feel fine today, they will be fine tomorrow. The purpose of insurance is to protect against the unpredictable, high-cost events that can derail your financial life in an instant.

The decision to forgo health insurance is a high-stakes gamble with your health and financial stability. In 2026, with medical costs continuing to climb, the potential downside is greater than ever. Proactively seeking coverage through the Marketplace, an employer, or a government program provides not just access to care, but also profound peace of mind and a critical buffer against life’s uncertainties. Investing in health insurance is, fundamentally, an investment in your future security.

Compare health plans

Finding plans in your area…