Living Without Health Insurance in California: 2026 Consequences

Understand the 2026 penalties and risks of being uninsured in California. For personalized guidance on your options, call our experts at (833) 877-9927.

By Monique Ashford

Compare health plans

Finding plans in your area…

As you look ahead to 2026, the question of what happens if you don’t have health insurance in California carries significant financial and personal weight. The landscape of healthcare coverage, penalties, and safety nets continues to evolve, making it crucial to understand the specific implications for the coming year. Going uninsured is not simply a matter of skipping monthly premiums, it is a calculated risk that exposes you to substantial medical debt, limited access to care, and potential state-mandated penalties. This comprehensive guide breaks down the real-world consequences, from emergency room bills to tax implications, and outlines the pathways to securing coverage before you face a medical crisis.

The Return of the Individual Mandate Penalty in California

One of the most direct financial consequences of being uninsured in California is the state’s individual mandate penalty. While the federal penalty was reduced to zero in 2019, California reinstated its own requirement for residents to maintain qualifying health coverage starting in 2020. This mandate remains firmly in place for 2026. If you go without health insurance for more than three consecutive months in a year, you will likely face a penalty when you file your state income taxes. The penalty is calculated in one of two ways: either a flat rate per adult and per child in your household, or a percentage of your household income, whichever is higher. For 2026, these amounts are subject to adjustment for inflation, but they will represent a significant added tax burden. This penalty is not a one-time fee, it accrues for each month you or your dependents lack minimum essential coverage. Understanding this penalty is a critical first step in evaluating the cost of being uninsured versus the cost of a plan.

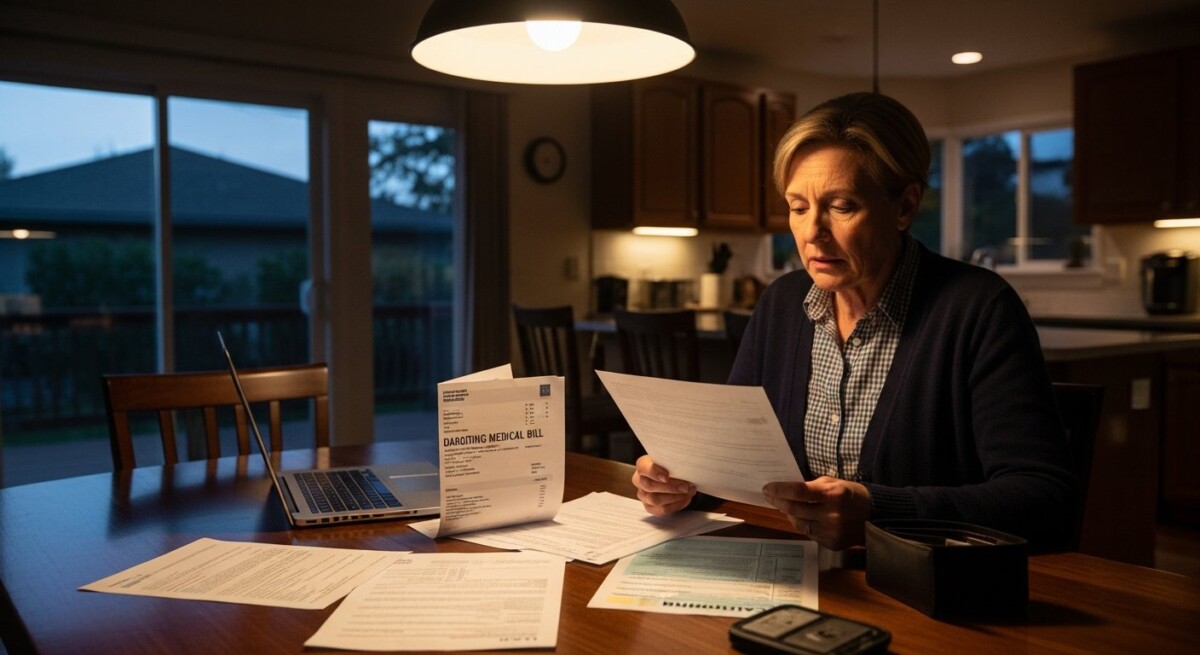

Financial Catastrophe: Facing Medical Bills Without Insurance

The state penalty, while substantial, pales in comparison to the potential financial ruin of a major medical event. Without health insurance, you are responsible for 100% of your healthcare costs. In California, these costs are notoriously high. A simple visit to an urgent care clinic can cost hundreds of dollars. An emergency room visit for a broken arm can easily exceed $3,000. More serious events, like an appendectomy or a multi-day hospital stay, can generate bills in the tens or even hundreds of thousands of dollars. Hospitals are required by federal law to stabilize patients in emergency situations regardless of ability to pay, but they will aggressively pursue payment for services rendered afterward. This can lead to collections actions, damaged credit, wage garnishment, and even bankruptcy. The financial risk is not hypothetical, it is a probable outcome for anyone who remains uninsured for an extended period. For a broader perspective on insurance options, our analysis of the best health insurance companies in the USA can provide a useful national context.

Limited Access to Care and Preventive Services

Beyond the bills, being uninsured severely limits your access to the healthcare system. You become a “self-pay” or “cash” patient. This often means you delay or forgo necessary care, including preventive services that can catch serious conditions early. You are less likely to have a primary care physician for routine check-ups, managing chronic conditions like diabetes or hypertension, or getting timely referrals to specialists. When you do seek care, you may face higher upfront costs, as many providers require payment at the time of service for uninsured patients. This creates a dangerous cycle: avoiding care due to cost leads to worsened health, which eventually results in a more expensive and acute emergency. Access to prescription medications is also severely restricted without the negotiated rates that insurance plans provide, making even common drugs financially out of reach.

The Challenge of Pre-Existing Conditions

If you develop a health condition while uninsured, securing coverage later can become more complex and expensive. Thanks to the Affordable Care Act (ACA), insurers cannot deny you coverage or charge you more based on a pre-existing condition if you enroll during an Open Enrollment period. However, if you try to enroll outside of Open Enrollment, you must qualify for a Special Enrollment Period (SEP), which typically requires a specific life event like losing other coverage, getting married, or having a baby. Without a qualifying event, you would be locked out of marketplace coverage until the next Open Enrollment, leaving you uninsured and managing a new health condition entirely on your own. This underscores the importance of not waiting until you are sick to seek coverage. For more on the rules for changing plans, see our detailed guide on when you can change health insurance plans.

Pathways to Coverage: Your Options for 2026

Fortunately, California residents have multiple avenues to obtain health insurance and avoid the consequences outlined above. The state’s robust marketplace, Covered California, is the central hub for most people. Here are the primary options available to you:

- Covered California (ACA Marketplace): This is where individuals and families can shop for qualified health plans (QHPs). Financial assistance in the form of premium tax credits and cost-sharing reductions is available based on your income, making coverage far more affordable for many. Open Enrollment for 2026 coverage will likely occur in late 2025.

- Employer-Sponsored Insurance: If you or your spouse has access to health insurance through an employer, this is often a cost-effective option. Be mindful of enrollment deadlines. If you experience a qualifying life event, such as getting married, you may be able to add a spouse to health insurance outside of the standard enrollment window.

- Medi-Cal (California’s Medicaid): This program provides free or very low-cost coverage to eligible low-income individuals, families, seniors, and people with disabilities. Eligibility is based on income and household size, and you can apply at any time of the year.

- Medicare: For individuals aged 65 and older, or those with certain disabilities.

- Catastrophic Health Plans: Available through Covered California to people under 30 or those with a hardship exemption. These plans have very low premiums but very high deductibles and are designed to protect against worst-case scenarios.

It is essential to compare these options carefully. While some may seek coverage from well-known providers, it’s important to understand the scope of different companies. For instance, you might wonder, does Geico have health insurance? The answer clarifies that they offer health insurance quotes through partners but are not a direct health insurer, highlighting the need to research your source of coverage.

Frequently Asked Questions

Is the California health insurance penalty enforced in 2026?

Yes, California’s individual mandate penalty is still in effect for 2026. You will report your coverage status and pay any applicable penalty when you file your 2026 state tax return in 2027.

Can I get health insurance anytime in 2026 if I’m uninsured?

No, you cannot. You can only enroll in a Covered California plan during the annual Open Enrollment period (typically November-January) unless you experience a qualifying life event that triggers a 60-day Special Enrollment Period. Medi-Cal accepts applications year-round.

What is the cheapest health insurance in California?

For those with very low incomes, Medi-Cal is often $0 premium. For others, the cheapest option is usually a Bronze-tier plan on Covered California, especially if you qualify for premium subsidies. Catastrophic plans are also low-premium but are only available to specific groups.

What if I can’t afford any marketplace plan?

If your income is below a certain threshold, you may qualify for Medi-Cal. If your income is slightly too high for Medi-Cal but you still find marketplace plans unaffordable, you should speak with a Covered California certified enroller. You may also explore whether you qualify for an exemption from the penalty due to unaffordability.

How does being uninsured affect my taxes?

When you file your California state income tax return (Form 540), you will need to indicate whether you and your dependents had qualifying health coverage for each month of the tax year. If you did not, you will calculate and pay the penalty as part of your tax liability.

The decision to forgo health insurance in California in 2026 is a high-stakes gamble with your health and financial stability. While the upfront cost of premiums may seem burdensome, it is a predictable expense that provides a critical safety net against the unpredictable and exorbitant cost of medical care. By exploring your options through Covered California, Medi-Cal, or employer plans, you can secure protection that ensures access to care, manages costs, and provides peace of mind. Taking proactive steps during an Open Enrollment period is the most powerful way to avoid the severe consequences of being uninsured.

Compare health plans

Finding plans in your area…