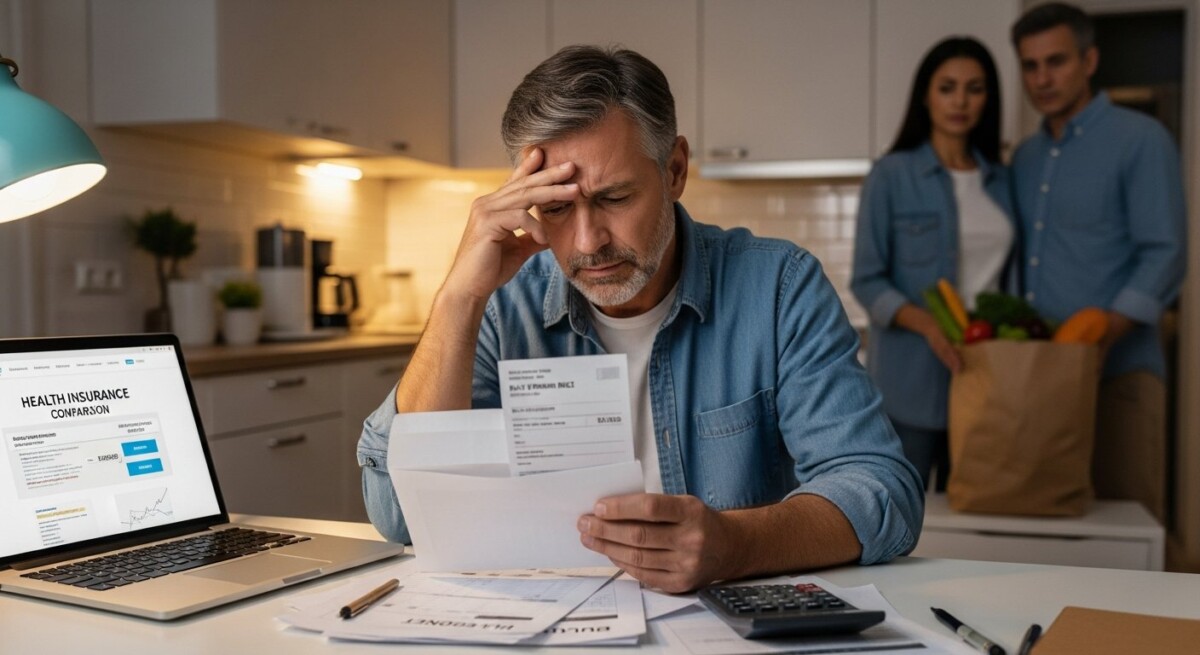

Imagine opening your mail or checking your bank statement and seeing a premium increase of 20, 30, or even 50 percent on your health insurance policy. Your first reaction might be panic. Your second thought is likely about how to afford this sudden financial blow. In the United States, insurance premiums can rise unexpectedly due to changes in your policy, your health status, or the broader market. Understanding exactly what happens and what steps you can take is critical to protecting your budget and your coverage.

When your premiums jump without warning, the immediate impact on your household cash flow can be severe. Many families budget tightly for monthly expenses, and a sudden increase can force hard choices between paying for insurance, groceries, or rent. But you are not powerless. There are concrete actions you can take to challenge the increase, find more affordable alternatives, or adjust your coverage to reduce costs. This article walks you through the entire process, from understanding why premiums rise to exploring your options for lowering them.

Why Do Insurance Premiums Increase Suddenly?

Insurance companies do not raise premiums arbitrarily, though it can feel that way. Several factors trigger sudden increases. The most common is a change in your personal risk profile. For example, if you were recently diagnosed with a chronic condition, started a high-risk job, or moved to a different zip code, the insurer may recalculate your premium based on the new risk. In the health insurance market, especially for individual plans, age, tobacco use, and location are key rating factors.

Another major reason is the insurer’s overall claims experience. If the company paid out more in claims than expected across its entire pool of policyholders, it may raise premiums for everyone in that pool to cover the deficit. This is called a market-wide rate adjustment and often happens after a severe flu season, a natural disaster, or during a pandemic. Additionally, changes in federal or state regulations can force insurers to adjust their pricing. For instance, if a state expands mandated benefits or if the Affordable Care Act’s risk adjustment program changes, premiums may shift accordingly.

Finally, your own policy details can cause a spike. If you switched from a high-deductible plan to a low-deductible plan, or added a dependent, the premium will naturally increase. Sometimes a sudden increase is actually a mistake in billing or a miscommunication about your coverage tier. Always review the explanation of benefits and the premium notice carefully before assuming the increase is legitimate.

Immediate Steps to Take After a Premium Increase

Do not ignore the notice. The moment you see a premium increase, take action to verify the amount and understand your options. Here is a step-by-step approach to handling the situation.

Step 1: Read the Notice Thoroughly. Insurance companies are required to send a notice explaining the change, the effective date, and the reason for the increase. Look for a section that says "Rate Adjustment" or "Premium Change." Note the percentage increase and the new monthly amount. Also check if the notice includes information about your right to appeal or switch plans.

Step 2: Contact Your Insurer. Call the customer service number on your insurance card or the notice. Ask them to explain the reason for the increase in plain language. If the reason seems unclear or unfair, request a supervisor. Keep a record of the call, including the date, time, and the name of the representative you spoke with.

Step 3: Compare Your Current Plan to Other Options. You may be able to switch to a different plan from the same insurer or from a competitor. Even if you are outside the annual Open Enrollment Period, a significant premium increase may qualify as a triggering event for a Special Enrollment Period. Check with the health insurance marketplace or a licensed broker to see if you can enroll in a new plan.

Step 4: File an Appeal if Necessary. If you believe the increase is based on incorrect information, such as an error in your age, location, or health status, file a formal appeal with the insurer. You can also file a complaint with your state’s insurance department. Many states have a consumer assistance program that can help you navigate the appeals process.

Step 5: Consider Subsidies or Tax Credits. If you purchase insurance through the ACA Marketplace, you may qualify for premium tax credits that can lower your monthly payment. A sudden increase in your premium could actually increase your subsidy, making the net cost more manageable. Use the marketplace’s subsidy calculator or speak with a certified enrollment counselor to see if you qualify.

How to Lower Your Premiums Without Losing Coverage

Reducing your premium does not always mean switching to a bare-bones plan. There are several strategies that can lower your monthly cost while still providing meaningful protection. One approach is to adjust your deductible. Plans with higher deductibles generally have lower premiums. If you are relatively healthy and have some savings set aside for emergencies, moving to a high-deductible health plan (HDHP) could save you hundreds of dollars per month.

Another option is to narrow your network. Preferred Provider Organization (PPO) plans offer flexibility but come with higher premiums. Health Maintenance Organization (HMO) plans or Exclusive Provider Organization (EPO) plans typically cost less because they restrict you to a specific network of doctors and hospitals. If your current providers are in the network, switching to an HMO can significantly reduce your premium.

You can also explore short-term health insurance plans, which are often much cheaper than ACA-compliant plans. However, these plans do not cover pre-existing conditions and have limited benefits. They are best used as a temporary bridge between coverage periods, not as a long-term solution. For families, consider removing a dependent who may qualify for separate coverage through a job, school, or government program like Medicaid or the Children’s Health Insurance Program (CHIP).

Finally, check if you qualify for a subsidy. Many people assume they earn too much to receive help, but the income limits for premium tax credits are higher than most realize. In 2026, households earning up to 400 percent of the federal poverty level may qualify. If your income has decreased since you last applied, you could be eligible for a subsidy that dramatically reduces your premium.

When to Shop for a New Plan

If your premium increase is more than 10 percent and your insurer does not offer a reasonable explanation, it is time to shop around. You can compare plans from multiple carriers using the health insurance marketplace or through a broker. Even if you are locked into your current plan for the rest of the year, a sudden increase might qualify you for a Special Enrollment Period (SEP).

What qualifies as a Special Enrollment trigger? According to federal rules, losing minimum essential coverage, moving to a new area, getting married, having a baby, or adopting a child are all qualifying events. A significant premium increase alone is not a standard SEP trigger, but some states have additional protections. For example, California and New York allow consumers to switch plans mid-year if their premium increases by a certain percentage. Check your state’s rules or consult with a licensed agent.

When comparing plans, do not focus solely on the monthly premium. Look at the total cost of coverage, which includes the deductible, copayments, coinsurance, and out-of-pocket maximum. A plan with a slightly higher premium but a lower deductible could actually save you money if you expect to use medical services. Also check the network to ensure your preferred doctors and hospitals are included.

If you are considering a switch, remember that you cannot be denied coverage or charged a higher premium due to a pre-existing condition for ACA-compliant plans. This protection applies regardless of how many times you change plans. For non-ACA plans like short-term insurance, pre-existing condition exclusions still apply, so read the fine print carefully.

Understanding Your Rights Under the Affordable Care Act

The Affordable Care Act (ACA) provides several consumer protections that can help you manage sudden premium increases. First, insurers cannot raise your premium based on your health status or medical history. They can only use age, location, tobacco use, and plan tier to set rates. If you suspect your increase is due to a health condition, you may have grounds for an appeal.

Second, the ACA requires insurers to spend at least 80 percent of premium dollars on medical care and quality improvements, rather than administrative costs or profits. This is called the Medical Loss Ratio (MLR) rule. If an insurer’s MLR falls below 80 percent, they must issue a rebate to policyholders. A sudden premium increase could be a sign that the insurer is not meeting the MLR standard, and you may be entitled to money back.

Third, you have the right to a clear explanation of any rate change. Insurers must provide a notice that is easy to understand and includes the specific reasons for the increase. If the notice is vague or misleading, you can file a complaint with your state insurance commissioner. Many states have rate review programs that can block or reduce unreasonable premium increases before they take effect.

Fourth, the ACA’s guaranteed issue provision means you can always buy a plan during Open Enrollment or a Special Enrollment Period, regardless of your health. This gives you leverage when negotiating with your current insurer. If they refuse to lower your premium, you can leave and find a better deal elsewhere.

Frequently Asked Questions

Can my insurance company raise my premium mid-year?

Yes, but only under specific circumstances. For ACA-compliant individual and family plans, premiums are typically locked in for the entire plan year. However, if you change your coverage level, add a dependent, move to a new area, or age into a new rating bracket (for example, turning 21 or 63), your premium can change mid-year. For employer-sponsored plans, premium changes usually happen at renewal, but some employers adjust contributions quarterly.

What if I cannot afford the new premium?

If you cannot afford the increase, you have several options. You can apply for a subsidy through the ACA Marketplace, switch to a lower-cost plan, reduce your coverage level, or explore government programs like Medicaid or CHIP. You can also contact your insurer to request a payment plan or a hardship extension. Do not simply stop paying the premium, as that will result in a lapse of coverage and potential penalties.

Will a premium increase affect my tax credits?

Yes. If you receive premium tax credits through the Marketplace, a sudden increase in your plan’s premium could actually increase the amount of your subsidy. This is because the subsidy is based on the cost of the second-lowest-cost silver plan in your area. If that benchmark plan’s premium goes up, your subsidy increases to keep your out-of-pocket cost stable. You should update your income and household information on the Marketplace to ensure your credits are accurate.

How do I appeal a premium increase?

Start by filing an internal appeal with your insurance company. The notice you received should include instructions on how to appeal. If the insurer denies your appeal, you can request an external review by an independent third party. Your state’s insurance department can also provide guidance and may intervene on your behalf. Keep all documents, including the original notice, your appeal letter, and any correspondence.

Take Control of Your Health Insurance Costs

A sudden premium increase can feel overwhelming, but it does not have to derail your financial stability. By understanding why premiums rise, knowing your rights, and exploring all available options, you can find a solution that fits your budget. Whether you choose to appeal the increase, switch to a different plan, or adjust your coverage level, the key is to act quickly and stay informed.

If you need personalized help navigating your options, consider speaking with a licensed health insurance broker. They can compare plans from multiple carriers and help you find the most affordable coverage for your situation. For expert assistance and a free quote, call (833) 877-9927. Our team at NewHealthInsurance.com is available to guide you through every step, from understanding your premium increase to enrolling in a new plan that meets your needs.

About Nathaniel Crowley

The maze of health insurance options can be overwhelming, so I make it my mission to cut through the confusion and help you find the coverage that actually fits your life and budget. I cover everything from comparing ACA Marketplace plans and Medicare options to navigating enrollment deadlines and understanding how subsidies or tax credits work for your specific situation. My background includes extensive research into state-specific health insurance regulations and the fine print of plan types like HMOs, PPOs, and Short-Term policies, which I break down into clear, actionable guidance. You can count on me to provide practical, up-to-date information that empowers you to make confident decisions, whether you're shopping for a family plan, exploring Medicare, or dealing with a qualifying life event.

Read More